From Homes to Holidays: How India’s Borrowing Boom Turned into a Spending Spree

From Homes to Holidays: How India’s Borrowing Boom Turned into a Spending Spree

India’s household debt landscape is witnessing a dramatic shift, with more borrowing now going towards consumption rather than building assets. Personal finance expert Pranjal Kamra recently highlighted this growing concern, noting that the average individual debt has risen by 23% in just two years. Even more worrying, over half of this debt is now being used for personal expenses instead of long-term investments like housing.

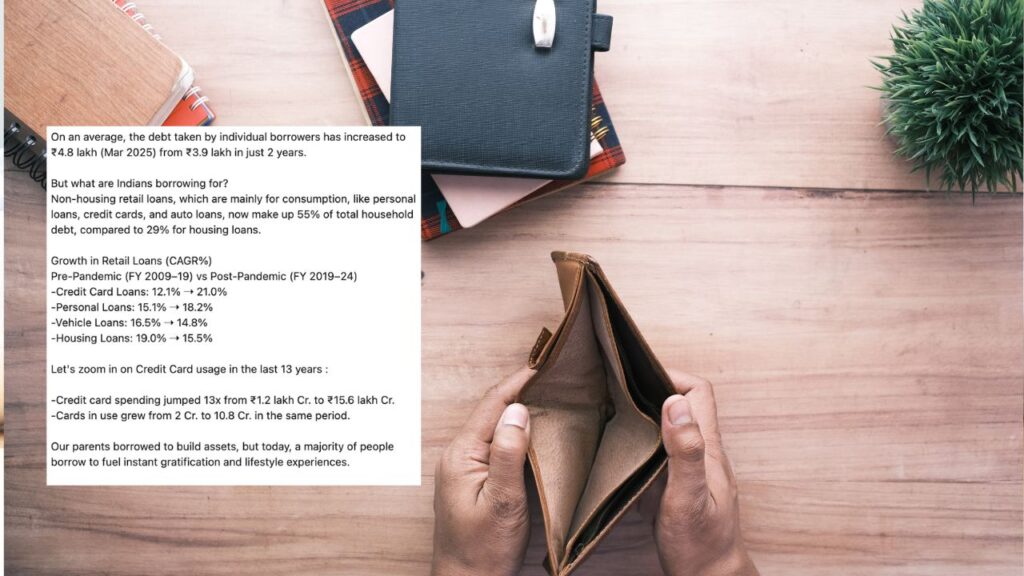

According to Kamra, the average debt per borrower has increased from ₹3.9 lakh in 2023 to ₹4.8 lakh as of March 2025. This jump comes alongside a clear shift in the purpose of borrowing. Non-housing retail loans, such as personal loans, credit card dues, and vehicle loans, now account for 55% of total household debt.

In contrast, housing loans make up just 29%, indicating that fewer people are borrowing to buy homes or build wealth.

Financial experts believe this shift represents a major change in how younger Indians are approaching money. Instead of using credit to acquire long-term assets, more people are opting for short-term satisfaction, spending on lifestyle choices, travel, and consumer goods.

Credit Card Usage Sees Explosive Growth

One of the most striking changes is in credit card use. In his post, Kamra points out that over the past 13 years, credit card spending has increased 13 times, from ₹1.2 lakh crore to ₹15.6 lakh crore. The number of credit cards in circulation has also surged, growing from 2 crore to over 10.8 crore during the same period.

Kamra also shared that this shows how consumer culture has evolved. Unlike earlier generations who focused on saving and asset creation, today’s borrowers are more inclined to spend first and think later. The post-pandemic years have seen particularly fast growth in unsecured loans, especially through credit cards and personal loans.

Check his post here.

Economists Raise Red Flags on Rising Unsecured Credit

Economists warn that while this kind of borrowing can temporarily boost the economy by increasing consumption, it could pose long-term risks. The rising share of unsecured credit may weaken household balance sheets, making families more vulnerable to financial stress or sudden income shocks.

In recent months, the Reserve Bank of India has also expressed concern, flagging the sharp rise in personal loan and credit card balances recently. Policymakers believe this trend needs close monitoring, especially if defaults begin to climb.