How One Decision Pushed a Pune Professional Into Rs 15 Lakh Debt

How One Decision Pushed a Pune Professional Into Rs 15 Lakh Debt

Financial experts say the case highlights how even stable incomes can be overwhelmed by unexpected emergencies without adequate financial planning.

By Vidhi Lalla

Pune: Pune-based professional earning a monthly salary of Rs 90,000 has become the centre of discussion on social media after his financial journey revealed how a single medical emergency gradually pushed him into a debt of nearly Rs 15 lakh.

The story, shared by a financial advisor on LinkedIn, has struck a chord with many people because it shows that debt is not always the result of reckless spending. Instead, it can develop slowly when unexpected expenses force families to rely on loans and credit cards.

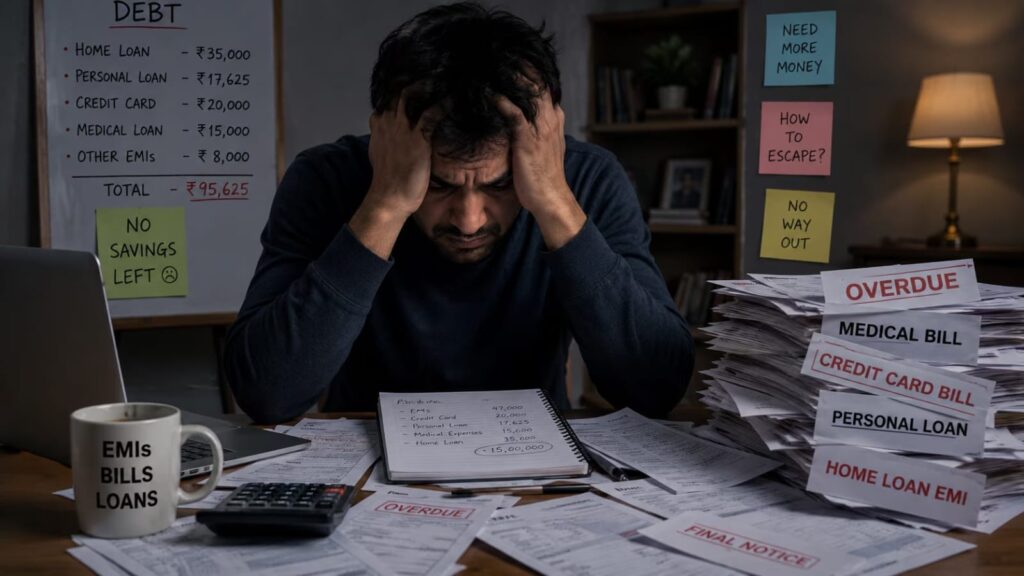

According to the post, the 36-year-old operations manager had been earning Rs 90,000 a month for three years. His household expenses were around Rs 82,000 every month, leaving only a small margin for savings. While his finances were tight, they remained manageable until his father required emergency surgery costing around Rs 5 lakh.

To arrange the funds, he decided to take a personal loan carrying an interest rate of 14 per cent. The additional EMI increased his monthly expenses from Rs 82,000 to nearly Rs 96,000, exceeding his monthly income and creating a recurring cash shortfall.

As the financial pressure mounted, he began using credit cards for daily household expenses such as groceries and fuel. Within a year, his outstanding credit card balance reportedly rose to around Rs 4 lakh. He later opted for another personal loan of Rs 6 lakh to consolidate the debt, but because his credit score had already declined, the new loan came with a higher interest rate of 18 per cent.

Instead of reducing the burden, the fresh loan only shifted the repayment pressure. Over the next two years, additional borrowing was used mainly to repay older loans, causing his total debt to rise to nearly Rs 15 lakh. According to the financial advisor, nearly 57 per cent of his monthly take-home salary, about Rs 51,000 was going towards EMIs alone.

The advisor noted that debt traps often begin when monthly loan repayments consume a large portion of one’s income. He suggested that individuals should treat EMIs exceeding 40 per cent of take-home salary as a warning sign and avoid taking fresh loans unless absolutely necessary.

The story triggered widespread discussion online, with many users sharing similar experiences. Several stressed the importance of building an emergency fund before it becomes necessary, saying that savings are far less expensive than borrowing during a crisis.

A discussion online followed the post, with users sharing their thoughts and lessons from similar experiences.

An individual wrote, “I always tell people, build an emergency fund before you need it. As it is much cheaper than borrowing later.”

Another posted, “The line about every new loan paying off the old one sums it up. By then, you’re no longer solving the problem, you’re just buying time.”

Others observed that debt usually grows through a series of small financial compromises rather than a single poor decision, while some pointed out that continuously taking new loans to repay existing ones only delays the problem instead of solving it.

A person commented, “Such an important reminder. I’ve seen that financial stress is rarely about one big mistake. It’s usually a series of small decisions made when options feel limited.”

Someone shared, “Debt spirals are rarely caused by one big mistake. They’re usually the result of small compromises made month after month.”

Tips to Avoid Taking Loans Beyond Your Budget

- Build an emergency fund that can cover at least six months of essential expenses.

- Keep total monthly EMIs below 40 per cent of your take-home salary.

- Avoid using credit cards to pay for routine expenses if you cannot clear the full bill every month.

- Compare interest rates carefully before taking any personal loan.

- Maintain adequate health insurance to reduce the financial impact of medical emergencies.

- Review your monthly budget regularly and cut discretionary spending before opting for new borrowing.

- Seek professional financial advice if debt repayments begin affecting essential household expenses.

Disclaimer: This article is based on a financial case shared publicly on social media. Individual financial situations vary, and readers should seek professional financial advice before taking borrowing or investment decisions.